Signals of Strength in a Shifting Economy

Four times a year, the U.S. Bureau of Economic Analysis (BEA) releases gross domestic product (GDP) estimates, measuring the total monetary value of all goods and services produced within the country. The BEA’s initial estimate for the first quarter of 2025 showed an unexpected contraction in real GDP, which is adjusted for inflation. This indicated a potential slowdown compared to the previous quarter.

GDP is driven by four main components: consumer spending, business investment, government expenditures, and net exports (exports minus imports). While a negative reading often raises concerns, the underlying data tells a more nuanced story. Encouragingly, consumer spending and capital investment, two key pillars of a market-driven economy, posted solid gains. The overall decline was caused by a modest drop in government spending and a sharp rise in imports. Because imports subtract from GDP, this increase is likely tied to recent tariff policy changes and possibly a one-time event, which weighed on the final number.

“A single negative GDP reading doesn’t tell the full story—strong consumer spending and business investment point to an economy that remains fundamentally healthy.”

Importantly, markets did not react with panic. The resilience of consumer demand and business investment suggests underlying economic health. Some investors may view the dip in government spending as a positive development, particularly in light of the federal deficit and today’s elevated interest rate environment. The rise in imports appears to be a temporary distortion rather than a lasting trend.

Looking ahead, pending legislative developments, including reconciliation bills and proposed tax reforms, could further support economic activity. These measures may boost employment and incentivize investment through expanded deductions and credits. It is also worth remembering that the BEA will revise this GDP estimate twice before finalizing it. Future adjustments could potentially reflect modest growth rather than contraction.

Ultimately, GDP is a lagging indicator. It reflects what has already occurred, not what is to come. For investors, the real takeaway is to view such data in context and avoid overreacting to short-term fluctuations in national output.

Tariffs

President Trump’s first 100 days in office have been eventful, to say the least. Tariffs continue to be the major focus and source of uncertainty. Much of the tariffs revealed on Liberation Day have been suspended for a 90 day period. And, although the Trump administration has been articulate that numerous negotiations are in progress, it seems unlikely that these negotiations would conclude within that 90 day period. Yet, the hope is that we start getting more and more clarity.

Trade-related negotiations with China have recently been a major development. Tensions between the US and China had escalated quite rapidly, resulting in tariff levels that were unsustainable and essentially would shut down any trade between the countries. Initially, China made efforts to meet with various countries in an effort to form alliances and discourage those countries from making deals with the US. Many other countries depend on the US in various ways, giving the US substantial leverage in certain negotiations. However, China isn’t in the same position. Yet still, China stands to lose many jobs if this tension isn’t resolved, and America stands to lose access to cheap manufacturing.

Neither China nor the US seemed willing to initiate communications initially. But finally, the countries began discussions and immediately agreed to pause most tariffs for 90 days. Specifically, US tariffs on most Chinese goods will be 30%, and China’s tariffs will drop to 10%. This is down from the over 100% tariffs that were previously in place. The clear message from both countries was that neither side wants a decoupling of trade. This was a major development on the global trade front, positively impacting financial markets and instilling more general confidence.

Another major trade development was the US’s announcement of its first trade deal since Liberation Day with the UK. Although the US will maintain a 10% baseline tariff on the country, there will be a reduction in trade barriers on many goods.

The Trump administration has started to focus more attention on a new tax bill, indicating that tariff-related revenue will allow for a reduction in taxes. We will likely see a continued focus on taxes until a new tax bill is finalized.

Economy

The economy has surely been impacted by the global trade developments, and we are now starting to see some of that in the economic data, namely the most recent GDP figures. First quarter GDP declined by 0.3%, the first contraction in 3 years. Interestingly, this was the result of surging imports, which are a reduction in the GDP calculation. This was clearly the result of expedited purchases ahead of the pending tariffs. The remaining components that form the GDP calculation were quite solid, and so it is a bit unusual to experience a negative GDP period within an economic expansion.

It’s important to remember that GDP is a backward-looking measure. It could be interpreted that the economy is resilient and able to withstand the uncertainty from global trade. Yet, the surge in imports could also indicate that consumers are highly concerned about the pending potential tariffs. Another consideration is that consumer confidence has been declining and fell again in April.

Aside from the recent GDP data release, there has been other cautiously optimistic support for a resilient economy. The International Monetary Fund recently released its outlook and expects tariffs to weaken the global economy but not cause a global recession. Further, the Trump administration is starting to focus more on deregulation and tax cuts with the goal of bolstering economic growth.

Monetary Policy

Powell’s consistent message in the wake of tariffs has been that the Fed needs to wait for greater clarity before continuing rate cuts. Some believed and hoped that the Fed might swoop in with lower rates to save the markets, but Powell was quite clear that this is not in the cards. He stated that markets are operating properly, and as one would expect given the unique trade-related developments and associated uncertainty.

Powell believes that global trade tensions could give rise to higher inflation and slower economic growth, which could pose some challenges for our country’s future monetary policy decisions. The Fed’s two priorities are inflation and employment, and these goals could come into conflict given the global trade developments. But the Fed has been clear that price stability is necessary for sustainable employment. There is still much dialogue around whether tariff-related inflation will prove to be transitory or longer-term. Certainly, that will be impacted by the outcome of the numerous trade deals currently being negotiated.

“While economic uncertainty has increased, the Fed noted that the economy continues to expand at a solid pace, with a strong job market and inflation only somewhat elevated.”

April Consumer Price Index data was just released and was below expectations and lower than the prior month. This was one of the lowest CPI readings in years and a welcome development in the wake of the global trade uncertainty. With that said, this likely won’t impact the Fed’s decision making process since much of the tariff-related pressure has likely not yet shown up in the inflationary data.

The labor markets softened in March, with job openings hovering near a four-year low. Yet in April, jobs data came in stronger than expected. This employment data isn’t conclusively positive or negative, so again, it likely won’t impact the Fed’s current stance.

As expected, the Fed held interest rates for the third meeting in a row, commenting that economic uncertainty has increased further yet continues to expand at a solid pace. The Fed also commented that it feels the job market is solid and that inflation is somewhat elevated.

One of the more publicized developments related to the Fed is Trump’s increasingly pointed criticism of Powell. Trump has recently made a series of public comments about Powell. It is abundantly clear that Trump believes Powell has been too slow to cut rates. Trump is also clearly eager to replace Powell in May of 2026.

Stocks

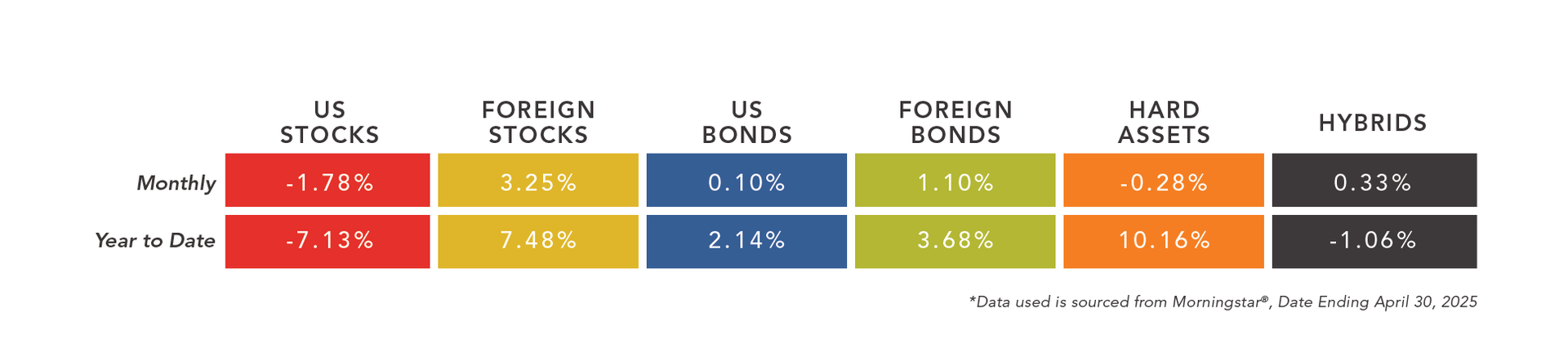

Stocks welcomed a series of positive developments recently, leading to a swift rebound from the lows experienced in early April. Two key announcements related to global trade were the US-China tariff pause and America’s first trade deal since Liberation Day. Further, employment and inflationary data were better than expected, which helped give stocks more confidence. Finally, Trump’s increasingly aggressive criticism of Powell led some to believe that Trump was striving to remove Powell prior to his term. This caused a spike in stock market volatility, but Trump later clarified that he did not have this intention, which calmed markets. Overall, the environment for stocks seems to be on a good trajectory, but surely faces more uncertainty.

Foreign stocks continue to show tremendous strength relative to the US markets. The international markets have been outperforming US stocks by a sizable margin since the beginning of the year. Foreign and US stocks now have generally equivalent three year average returns, which has been quite the comeback for foreign markets.

From a market cap perspective, small caps in the US have underperformed their large cap counterparts. Small caps are generally more susceptible to interest rate pressures, which have been heightened due to the Fed’s pause on interest rate cuts. Interestingly, foreign small caps have generated sizable returns since the beginning of the year.

Bonds

The returns experienced in the broad bond markets were split during the month of April. Treasuries with shorter maturities performed well, whereas longer-term Treasuries declined. Long-term bonds are still trying to claw back returns from the Fed rate hike cycle, which led to rather significant declines for these interest-sensitive bonds. Many of these long-term bonds have large negative annualized returns over quite a long time period. Shorter term bond yields are currently being preserved as the Fed maintains its stance on interest rates. This is a good thing for savers who are looking to maximize interest on short term reserve funds.

Higher-yielding bonds have been generally flat since the beginning of the year but still hold on to attractive, longer-term total returns. Yet, there are some growing concerns that the new tariffs will impact high-yield bond issuers’ ability to repay debt in the future. This is another implication of tariffs that needs to be closely monitored.

Foreign bonds have generally been more resilient than US bonds during tariff-related developments. Certain foreign bond markets have experienced very strong returns since the beginning of the year, many of which have doubled the total returns of similar US treasury bonds.

© Advisory Alpha. Registration with the SEC or state does not constitute an endorsement of the firm by regulators, nor does it indicate that the adviser has attained a particular level of skill or ability. This content is for informational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. Investing involves risk, including the potential loss of principal. No investment strategy, such as asset allocation or diversification, can guarantee a profit or protect against loss in periods of declining values. All investment strategies involve risk and have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions may materially affect the performance of your portfolio. There are no assurances that a portfolio will match or outperform any particular benchmark. Investors should carefully consider the investment objectives, risks, fees, and expenses before investing. Any financial services firms referenced in this material do not provide tax or legal advice. Please consult with your tax or legal professional regarding specific issues prior to making a tax or legal decision.

The performance information presented in the asset category section of this report is based on equal-weighted averages of the following Morningstar Categories: US Stocks (US Fund Large Blend, US Fund Mid-Cap Blend, US Fund Small-Blend), Foreign Stocks (US Fund Foreign Large Blend, US Fund Foreign Small/Mid Blend, US Fund Diversified Emerging Mkts), US Bonds (US Fund Intermediate Government, US Fund Inflation-Protected Bond, US Fund Corporate Bond, US Fund High Yield Bond, US Fund Bank Loan), Foreign Bonds (US Fund World Bond, US Fund Emerging Markets Bond), Hard Assets (US Fund Commodities Precious Metals, US Fund Commodities Energy, US Fund Global Real Estate, US Fund Real Estate), Hybrid Assets (US Fund Convertibles, US Fund Preferred Stock).

© 2025 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. Morningstar category data is provided for illustrative purposes only to demonstrate a hypothetical investment vehicle represented by a group of similar investments. Morningstar category data is an aggregation across actual funds contained in the category, but it is not possible to directly invest in a category. Index returns are provided for illustrative purposes only to demonstrate a hypothetical investment vehicle using broad-based indices of securities. Unmanaged indexes are not available for direct investment. All data shown does not include internal fund expenses, trading costs, financial advisor fees or commissions, or taxes. This information is not intended to predict the performance of any specific investment or security. Past performance is no guarantee of future results.

Bureau of Labor Statistics. Unemployment Rate, Total Nonfarm Employment, Labor Force Participation, Consumer Price Index, Producers Price Index. www.bls.gov. United States, Department of Commerce, Bureau of Economic Analysis. Personal Consumption Expenditures, Gross Domestic Product, Consumer Spending, Personal Income and Outlays. www.bea.gov. Federal Reserve. Fed Funds Rate, Fed Funds Target Range, Minutes of the Federal Open Market Committee, Board of the Federal Reserve System Calendar. www.federalreserve.gov. Trump, Donald. @realDonaldTrump. Truth Social.